China Will Provide 2.5 Trillion for Tax Rebate and Reduction

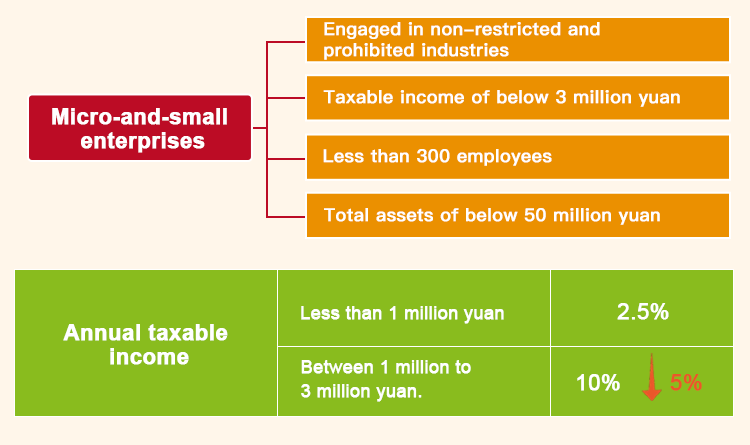

The preference of 3% to 1% for small taxpayers will be maintained, while the VAT exemption is expected to be increased to 200,000 yuan on monthly sales or 600,000 yuan on quarterly sales.

![]()

![]()

![]()

![]()

![]()

![]()

The preference of 3% to 1% for small taxpayers will be maintained, while the VAT exemption is expected to be increased to 200,000 yuan on monthly sales or 600,000 yuan on quarterly sales.