Bank Closed, Tax Rejected: A Survival Survey of Singapore Co. in 2026

The landscape for cross-border business in 2026 has irrevocably shifted. The era of aggressive tax optimization and opaque structures is over. We have entered a period defined by unparalleled transparency and rigorous regulatory enforcement, moving from a primary focus on “tax savings” to an urgent need for “compliance defense.”

Recently, our advisory team has been inundated with urgent distress calls from entrepreneurs and corporate owners with operations in Singapore. The narratives are alarmingly similar:

● “We spent a significant amount of money and time to set up our Singapore entity. The business is running, the ink on our online banking application is barely dry, yet the bank is demanding an exhaustive chain of documentation tracing everything back to our Ultimate Beneficial Owners (UBOs). Why?”

● “Our corporate account has been active for three years with pristine, legitimate transaction volume. Out of nowhere, we received a curt notice from the bank: ‘Account Closure in 30 Days.’ Why us? What did we do wrong?”

In the past, the dominant discourse centered on utilizing offshore structures for profit maximization and leveraging Singapore’s competitive basic corporate tax rate of 17%, enhanced by substantial tax exemptions for the first three years for qualifying private companies (PTEs).

Today, however, the rules of engagement are different. Operating a Singapore company with a “shell company mindset”—a focus on minimal local activity and maximum global profit-shifting—is a formula for structural and financial collapse. Many entrepreneurs fail to grasp that a bank account closure is rarely the root issue. Rather, it is the visible symptom of a global regulatory crackdown on non-compliant, opaquely held assets.

【Deep Policy Dissection: The Regulatory Perfect Storm】

Why has Singapore become so seemingly “inhospitable” to foreign business structures in 2026? This seismic change is not a whim but the result of a coordinated convergence of four powerful regulatory and policy initiatives.

1. The Implementation of the “Corporate Service Providers Act”

By 2026, Singapore’s commitment to Anti-Money Laundering (AML) has reached its peak regulatory apex. The Monetary Authority of Singapore (MAS) is now exerting intense pressure directly on all financial institutions and licensed Corporate Service Providers (CSPs) – the very secretaries, auditors, and lawyers who help establish companies.

This intense regulatory scrutiny has caused banks and CSPs to adopt an “overly cautious” stance. The cost of non-compliance—including astronomical fines and irrevocable reputational damage—means they will proactively reject or close any account or entity with even a trace of compliance defect. In this environment, a policy of “better safe than sorry” reigns supreme.

2. Full Implementation of BEPS 2.0 (Global Minimum Tax)

The year 2026 marks the full, global implementation of the 15% Global Minimum Corporate Tax (Pillar 2) in major jurisdictions, including both Hong Kong and Singapore. While this “15% rule” primarily affects large Multinational Enterprises (MNEs) with group-wide revenue exceeding €750 million, its ripple effect on Small and Medium-Sized Enterprises (SMEs) and entrepreneurs is significant and underestimated.

To maintain their own global compliance and audit standards, major multinational corporations are now requiring all companies in their entire supply and distribution chain—meaning thousands of SMEs—to provide a comprehensive, documented, and verified history of their tax residency and compliance. If your structure is opaque, you will fail their risk assessments and be locked out of key supplier databases and business partnerships.

3. The CRS 3.0 “Upgraded Storm”

The Common Reporting Standard (CRS), already in full effect, has been upgraded to CRS 3.0. This new iteration has been specifically designed to capture wealth held in crypto-assets and global insurance policies, which were previously effective shelters. With the Automated Exchange of Information (AEOI) protocols at maximum efficiency, Singapore’s financial network is now a global information conduit, exchanging a wider array of asset data than ever before. This includes rigorous, look-through analysis to identify and report the real owners behind all types of corporate entities and investment vehicles.

4. The “Strong Binding” of Identity and Wealth

Current market dynamics have evolved past a fragmented view of “migration” and “tax planning.” The new paradigm is the strategic fusion of identity planning and financial compliance. For high-net-worth individuals and families using Wealth Management to secure residency (e.g., through Singapore’s Family Office framework: VCC / Section 13O / Section 13U), the bar for entry is now consistently set at S$20 million (or higher). This permanent high threshold forces a profound strategic question: Beyond the tax incentives, what other compliant advantages does your Singapore Family Office provide in 2026?

🔗 News/Policy Alert: The Monetary Authority of Singapore (MAS) has recently announced aggressive enforcement actions. Within this year alone, it has revoked the licenses of dozens of Corporate Service Providers for AML violations. Furthermore, MAS has mandated that all local banks conduct a comprehensive.

comparative chart showing the sharp rise in MAS-directed AML enforcement actions versus the rising trend line for corporate bank account opening difficulty in Singapore (2020-2026)

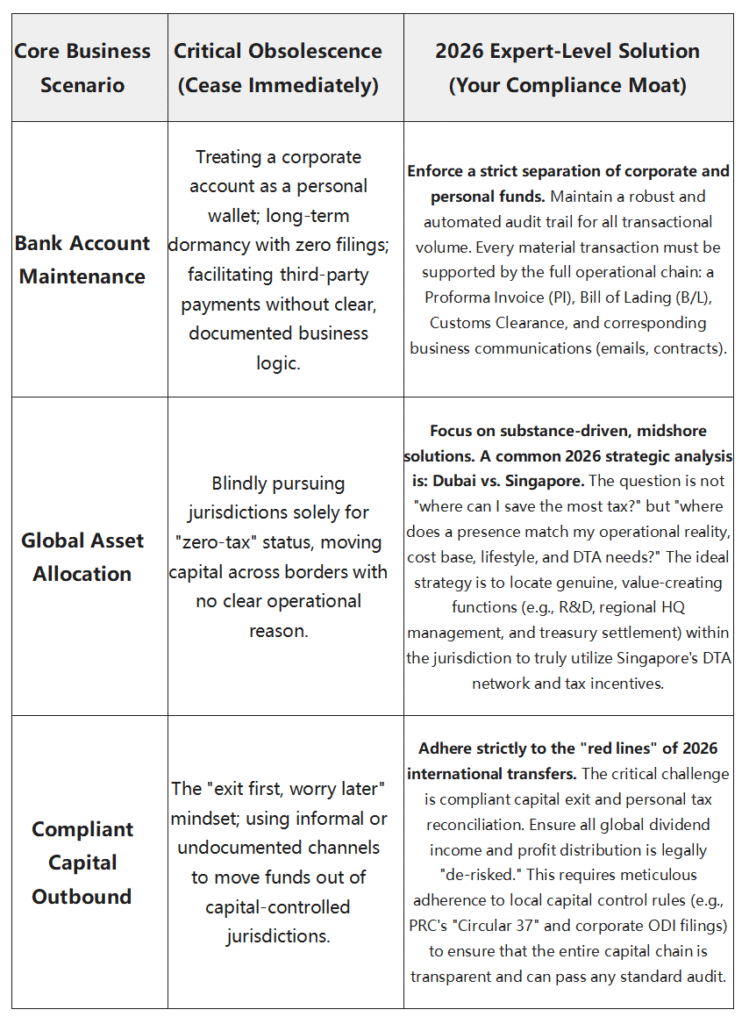

【Real Case Analysis: Where is Your Financial Bomb?】

To illustrate the visceral, real-world impact of these new compliance standards, here are three critical “emergency room” cases my team has handled recently:

Case 1: The E-Commerce Owner’s “Asset Commingling” Disaster

● Background: Mr. Zhang, an owner of a successful independent cross-border e-commerce brand, established his Singapore company in 2023. For personal convenience, he routinely commingled business and personal funds. He frequently used the Singapore corporate account for personal “living expense” transfers for himself and his family, and occasionally, “as a favor,” accepted a few third-party international trade payments of unclear origin.

● The 2026 Outcome: In early 2026, these actions triggered the automated AML risk models of his Singapore bank. The bank demanded that Mr. Zhang provide a full transactional audit: original business contracts, corresponding Bills of Lading (B/L), and all relevant customs declarations for every single large transaction. Because the transaction narrative didn’t match the documentation and included personal expenses, he could not reconcile the account. The account was forcibly closed, nearly S$1 million in capital was frozen, and he was added to an inter-bank risk blacklist, making it all but impossible for him to open a new account in another Singapore financial institution.

Case 2: The Traditional Manufacturer’s “Pure Shell” Backlash

● Background: A large PRC-based machinery manufacturing company utilized its Singapore subsidiary purely as an “Invoicing Center” to aggregate profits. It had a corporate address but maintained no physical office in Singapore, employed zero local staff, and incurred virtually no genuine operational expenses in the jurisdiction.

● The 2026 Outcome: During the 2026 annual review, the bank and Corporate Service Provider demanded documented proof of Economic Substance (ES). Since the company was a quintessential mailbox company, it could not meet the test. The company is now exposed to a severe audit and a finding of Controlled Foreign Corporation (CFC) status by PRC tax authorities, which would lead to a massive back-tax assessment on those profits. Furthermore, the Singapore Inland Revenue Authority (IRAS) has flagged the entity as “high-risk,” and it has retroactively lost all benefits and exemptions under Singapore’s extensive network of Double Tax Agreements (DTAs).

Case 3: The Technology Founder’s “Complex Structure” Deadlock

● Background: The founder of a tech company, following obsolete and flawed advice, built an intricately complex red-chip structure involving multiple offshore entities: BVI -> Cayman -> Singapore -> China OpCo. The structure was designed with the sole purpose of completely obscuring the final beneficial owner (the founder).

● The 2026 Outcome: The bank in Singapore demanded a direct, complete, and verifiable path through to the UBO. The founder was unable to satisfy the bank’s KYC requirements, which included providing full documentation of the BVI and Cayman entities’ compliance with their own local Economic Substance laws. The red-chip structure’s complexity had become its own fatal obstacle. The structure did not save any tax and, in fact, saddled the founder with astronomical, non-deductible maintenance fees for a structure that the Singapore bank would not and could not accept. The new mantra: Simplicity and Transparency are the only compliant solution.

【Strategic Overview: A Compliance Moat for 2026】

The difference between successful and failing operations in 2026 lies in your adherence to a new compliance standard. This is no longer optional; it is survival.

In the intense compliance context of 2026, “obfuscation” is no longer a tool to protect wealth; it is a liability that invites risk. “Transparency and compliance” are now the most expensive, yet the most indestructible, moats a cross-border enterprise can possess.

To achieve long-term security and enduring operations in Singapore—and indeed in any of the world’s leading financial centers—you must operate from a foundation of truth. Accept compliance costs not as an unwelcome expense, but as your company’s most important strategic investment. Match your financial and tax structure with your genuine, verifiable business operations. This is the only true way to navigate this new age, ensure resilience, and build a truly enduring, global enterprise.