一文详解新加坡企业所得税

新加坡经济蓬勃发展,并且有一流的金融中心策略位置。在说起充满活力的新加坡商业环境时,新国的公司税率往往是首个重点话题。其税率制度有效率,并且有各种税收优惠,加上新加坡企业所得税税率降低,都是吸引外资进入新国的原因。

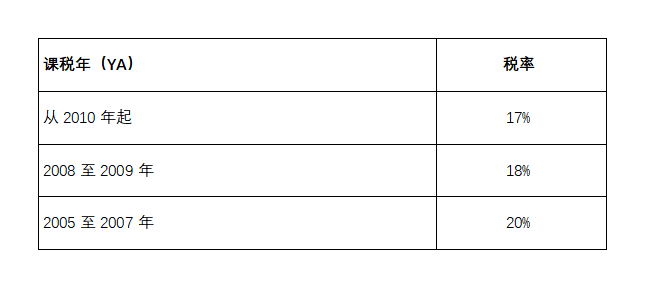

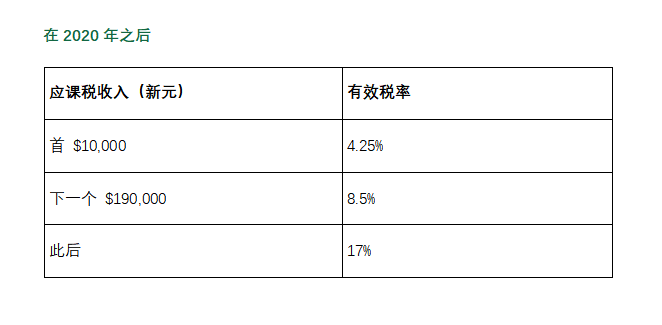

新加坡经济蓬勃发展,并且有一流的金融中心策略位置。在说起充满活力的新加坡商业环境时,新国的公司税率往往是首个重点话题。其税率制度有效率,并且有各种税收优惠,加上新加坡企业所得税税率降低,都是吸引外资进入新国的原因。公司税率 从2010年课税年开始,新加坡公司不论是本地公司还是外国公司,其应纳税收入均按17%的税率征税。

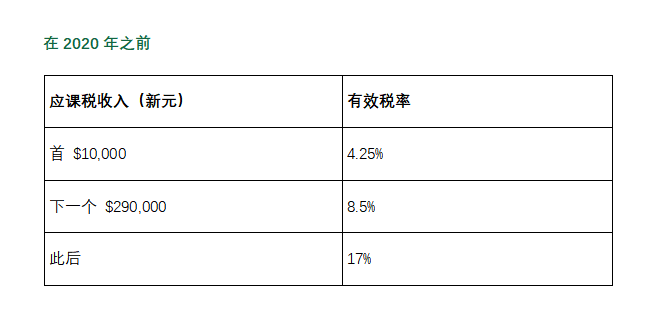

任何符合条件的新注册的公司(如下所述)都有权享受前三年新创办公司的每年的免税待遇税务评估。资格条件如下: increase the scheme allowance

- 在新加坡注册成立

- 在新加坡居住税

- 拥有不超过20名股东,其中至少一名股东是持有至少10%普通股的个人股东。

- 除这两类公司外,所有新公司均可享受免税待遇:

- 主要从事投资控股业务的公司;

- 一家从事房地产开发销售,投资或投资和销售的公司。

S$30,000 to S$50,000. At the same time, start-up business owners must raise S$10,000 themselves as Common matching funds for this allowance.

S$30,000 to S$50,000. At the same time, start-up business owners must raise S$10,000 themselves as Common matching funds for this allowance.Application conditions

3 SC/PRs and is the main applicant for funding

3 SC/PRs and is the main applicant for funding

公司的部分税务豁免 2 of the 3 main applicants are first-time founders

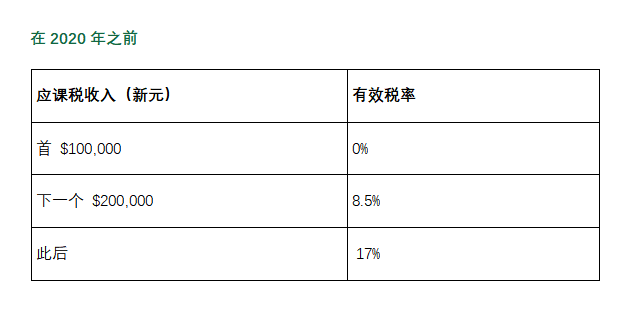

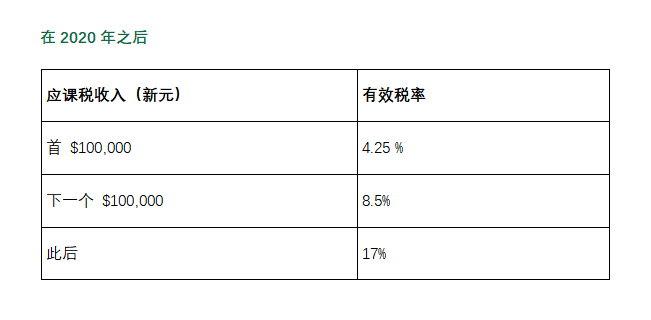

公司在其第4个纳税评估年度以及所有其他公司将有权无限期享受部分免税待遇。

6 months

6 months

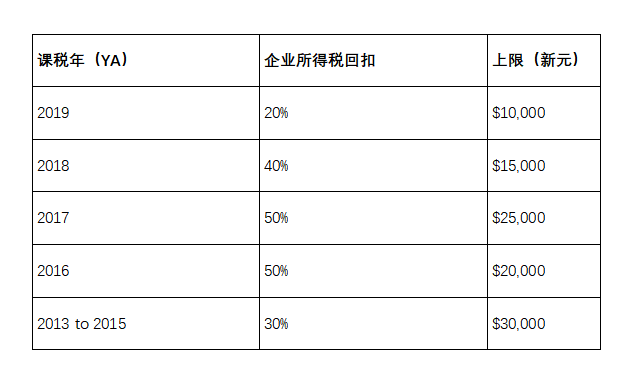

一次性企业所得税(CIT)回扣

根据新加坡财政预算案公告,每家新加坡公司都有资格获得CIT退税。以下是可申请各税务评估年度的CIT回扣:

新加坡公司税务指南

S$250,000 and S$500,000 01 新加坡公司的 “新公司免税(SUTE)计划” 10% and 20%, respectively, based on their POC and POV grants.Application conditions

所需资格包括: 5 years at the time of grant application

i. 不超过20名股东 ii. 一人必须持有至少10%的分发股权(就公司股东而言) iii. 房地产和投资控股公司不符合资格

尽管自2010年以来,新公司免税(SUTE)计划把担保型公司涵盖在内,但给予新公司的免税计划并未不包括2013年2月以后成立的投资控股公司和从事房地产开发活动的公司。 S$100 million or group employees not exceeding 200

POC or POV program categories: Advanced Manufacturing/Robotics, Biomedical and Healthcare, Cleantech, ICT, Emerging Industries, Precision Engineering, Transportation Engineering/Engineering Services, Food Science and Technology, and Agritech

(For other detailed terms, please refer to ESG’s official website)

Local Company

Specific industries covered by PSG include retail, food, logistics, precision engineering, construction, and landscaping. In addition to industry-specific solutions, PSG supports the adoption of cross-industry solutions such as customer management, data analysis, financial management, and inventory tracking.These solutions have been pre-determined by various government agencies such as Enterprise Singapore (ESG), National Environment Agency (NEA), and Singapore Tourism Board (STB).

The scheme grant is capped at S$30,000 per financial year. From April 1, 2022, the highest support level will be at 70%. For eligible pre-determined solutions in the food service and retail industries, the government provides an additional 10% of the maximum level of support, or 80%, until 31 March 2023.

Application conditions

SMEs who meet the following conditions can apply for PSG:

A business entity registered and operating in Singapore

Own at least 30%local equity (for selected solutions only)

At least three local employees at the time of application (for Consulting Services Solutions only)

Purchase/rental/subscription of IT solutions/equipment/consulting services must be used in Singapore

Corporate group annual sales of not more than S$100 million, or corporate group employees not exceeding 200

b. Overseas business development: such as participating in overseas physical and virtual trade fairs or business matching, identifying licensees/franchisees, distributors or joint venture partners, etc.; capped at S$50,000

c. Overseas establishment: includes legal and documentation fees to enter the market, as well as in-depth free trade agreement consultation, etc.; capped at S$30,000

There is no limit to the number of MRAs a company can apply for. Only one activity can be funded at a time for a maximum period of 12 months. Companies can also apply for other grants at the same time.

Application conditions

03部分免税(2017年)

A business entity registered and operating in Singapore

为了帮助企业应对成本上升、经济不明朗问题,并且有能力进行调整,所有公司都有资格获得企业所得税回扣,其中2017课税年的回扣上限将从$20,000增加到$25,000新元。回扣率将维持在公司应缴税的50%。此外,CIT回扣将得到加强和扩展如下: a)对于YA2018,CIT回扣将提高到应纳税额的40%,增加上限为15,000美元 b)CIT退税额度将延长一年至YA2019,税率为20%,最高限额为10,000美元

Own at least 30% local equity

Corporate group annual sales of not more than S$100 million, or corporate group employees not exceeding 200

04企业的外国来源收入豁免条款: These types of programs help businesses prepare for growth and transformation by strengthening their business foundation. These projects should go beyond basic functions like sales and accounting.

b. Innovation and Productivity汇入新加坡的外国收入应在新加坡纳税。然而,新加坡所得税法(ITA)第13(7A)至13(11)条文说明,公司可以从外国来源的收入豁免计划(FSIE)中受益。(请注意,该海外国家的公司税率需至少是15%,并且该笔收入已经在该海外国家纳税,豁免计划才可行。)

c. Market Access外国来源收入类别:

i. 来自海外的股息 – 来自海外的股息。如果是由非新加坡税务居民公司支付。 an additional 10% of the maximum level of support, or 80%, until 31 March 2023.

Application conditions

ii. 外国分行的利润 – 新加坡公司在外国注册分行所产生的任何利润。不适用于外国分行的非贸易或非生意性质收入。

A business entity registered and operating in Singapore

Own at least 30% local equity

iii. 来自海外的服务收入 – 居民纳税人通过在海外的固定营运场所提供的服务所产生的任何收入。

Enterprise Singapore will assess applications based on project scope, project outcomes and the capabilities of the service provider.

Application conditions

i. 双重税务减免(DTR) – 新加坡已经签署了20多项自由贸易协定(FTA),以及74个全面的和8个有限的避免双重税收协定(DTA),以促进跨境贸易,并使到在新加坡的公司减轻他们的海外扩充的成本。因此,双重税务减免(DTR)是避免双重税收协定(DTA)提供的减免,以抵消双重征税状况。

A business entity registered and operating in Singapore

Own at least 30% local equity

Corporate group annual sales of not more than S$100 million, or corporate group employees not exceeding 200

ii. 单边税收抵免(UTC) – 在没有避免双重税收协定(DTA)的地方,如果有以下情况汇入的收入,则允许单边税收抵免(UTC):

· 来自专业、咨询和其他服务的收入 · 版税收入 · 股息收入 · 就业收入 · 分支利润

Workforce Transformation: SkillsFutureSingapore (SSG), Job Redesign Programme, Career Switching Programme etc. Training courses aligned with various industry skills frameworks provided by Workforce Singapore (WSG)

To encourage employers to undertake both enterprise and workforce transformation programmes, the S$3,000 credit can only be used for workforce transformation programmes. Therefore, employers can only use up to S$7,000 for business transformation, and there is no cap on the amount that can be used for workforce transformation.

Application conditions

Employers must meet the eligibility criteria for individual SFEC support programs in order to withdraw credits.

Employers who are newly eligible in 2021 can use their SFEC for supportable programs applying from 1 April 2022. Employers who were previously eligible can continue to use their SFEC for supportable plans submitted on or after April 1, 2020.

Final reimbursements for SFEC support programs must be submitted to the respective agencies by June 30, 2024.

Partnership

LEAD supports development projects in the following areas:Technology and Infrastructure: Improve business capabilities and productivity through the use of technology to innovate and automate. It includes adopting technology, setting technical standards and building industry-wide infrastructure

Industry expertise: Develop overall industry expertise through training, study circles and industry certifications

Business cooperation: Encourage associations and businesses to build alliances by leveraging mutual strengths through joint procurement, shared services and internationalization opportunities

Intelligence and Research: In-depth understanding of industry trends and needs to develop industry-specific solutions through comprehensive research based on sound market intelligence

Internal capabilities: Strengthen internal capabilities to be effective change agents and industry multipliers

LEAD provides reimbursement of up to 70% of eligible costs for eligible projects, including labor-related costs, equipment and materials, professional services, business development costs, and intellectual property costs.

High-impact and multi-TAC collaborative projects can receive up to 90% support. Models for multi-TAC partnerships include collaboration within and across industries, or alliances where large TACs take the initiative to engage and support smaller TACs to achieve common outcomes.

Application conditions

LEAD applies only to trade associations and chambers of commerce TAC, which include Singapore registered associations, professional bodies, employers’ unions, overseas chambers of commerce, and companies limited by guarantee.

The TAC must also meet the following criteria:

Represents a key industry (i.e. an industry that contributes significantly to the economy, has good export potential, and a strong employment scale)

Has a large membership representing the industry

Proven track record in helping small and medium enterprises (SMEs)

The proposed project must be started at the time of application

From 1 January 2017, TACs seeking consultancy-related costs for LEAD support in their industry development projects are required to engage management consultants with Enterprise Singapore accredited accreditation.