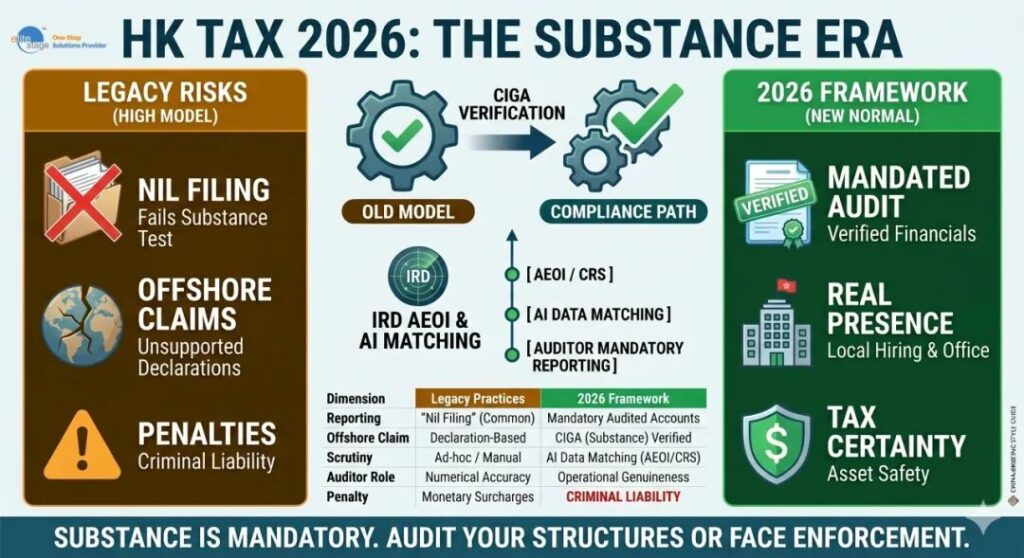

Compliance Alert 2026: The Death of “Nil Filing” for Hong Kong Offshore Claims and the Rise of Criminal Liability

In the regulatory landscape of 2026, the era of “strategic ambiguity” for Hong Kong offshore structures has reached a definitive end. For years, many investors and international traders relied on “Nil Filing” (zero-tax reporting) or superficial offshore claim applications—often facilitated by unscrupulous secretarial firms—to bypass tax obligations.

As BEPS 2.0 Pillar Two becomes the global baseline and Hong Kong’s tax authorities (IRD) adopt AI-driven, cross-border data matching, the net has closed. Investors still operating under the “old-school” assumption that a lack of physical presence equals a lack of tax liability now face more than just financial adjustments; they face the very real prospect of criminal prosecution for providing false information to the Inland Revenue Department.

01 Policy In-depth Deconstruction

As of 2026, the “Substance over Form” principle is no longer a guideline—it is a mandatory enforcement mechanism:

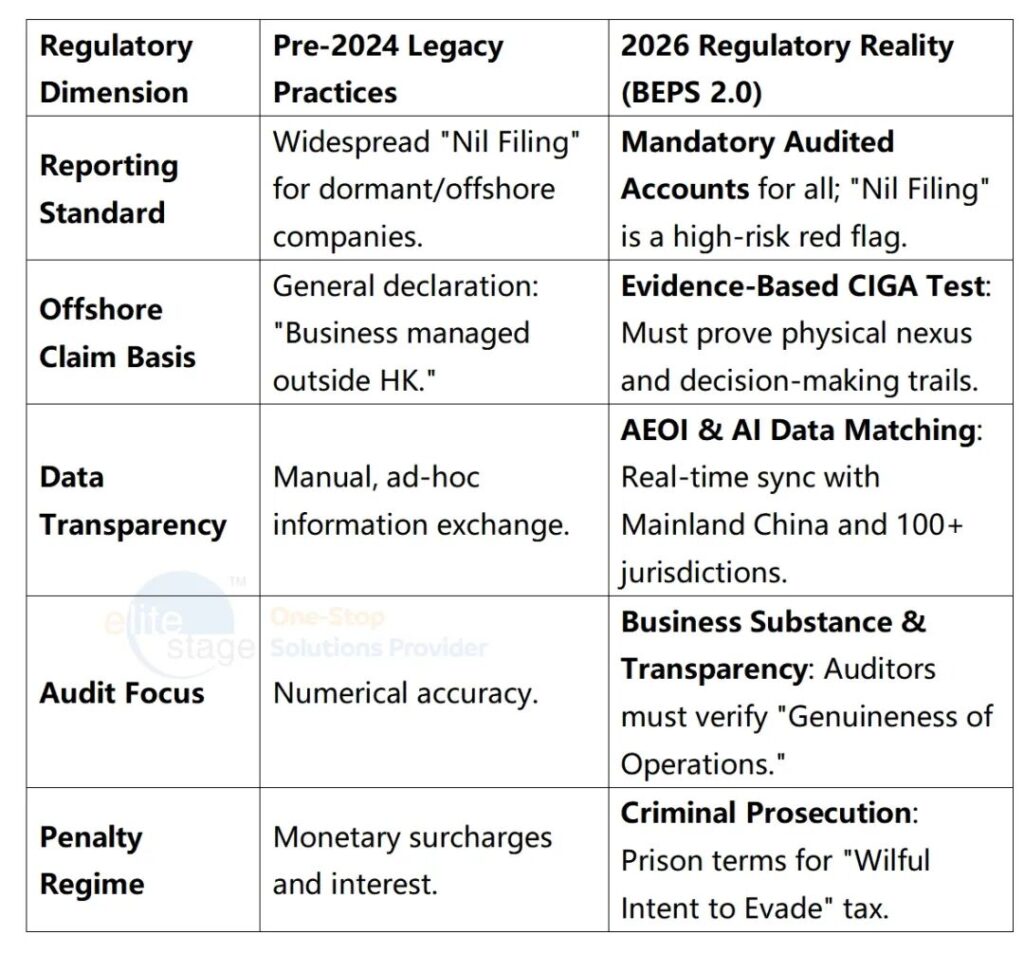

● The End of the “Nil Filing” Loophole: The IRD now requires all corporations, regardless of their activity level, to submit audited financial statements alongside their profits tax returns. The traditional “dormant” status is under intense scrutiny.

● FHTP & Modified Territorial Regime: Following the full integration of the Foreign-Sourced Income Exemption (FSIE) regime, passive income (dividends, interest, IP income) and even active trading profits are only exempt if the company can prove Core Income Generating Activities (CIGA) were performed in Hong Kong or that the profits were taxed elsewhere at a sufficient rate.

● Auditor Accountability (Criminal Nexus): Under the latest 2026 amendments to the Inland Revenue Ordinance, auditors are under a statutory duty to report “suspicious tax arrangements.” Any audit report found to be deliberately misleading or based on fabricated evidence (such as fake shipping documents to prove offshore status) will trigger joint criminal investigations into both the directors and the service providers.

02 2026 Compliance Reality: The Hong Kong Tax Shift

Practical Advice Steps for 2026 Compliance:

Immediate Substance Mapping: Document exactly where every contract is signed, where staff are located, and where the bank account is managed. If these occur in China, the offshore claim is likely invalid under 2026 rules.

Voluntary Disclosure: If you have historically filed “Nil” while having active business, consult with a Tier-1 tax firm for voluntary disclosure before the IRD’s AI detection system flags your account. Penalties are significantly reduced for self-rectification.

Restructuring CIGA: If you wish to maintain Hong Kong tax benefits, you must “onshore” your operations. This means hiring local qualified staff and renting physical office space to meet the CIGA requirements.

Don’ts:

● DO NOT trust “low-cost” secretarial firms promising 100% tax exemption for a flat fee. These are often the first to be blacklisted by the IRD.

● DO NOT provide inconsistent data. The IRD now cross-references your bank movement data with your customs/shipping declarations.

● DO NOT ignore “Query Letters.” In 2026, a failure to respond within 21 days can trigger an automatic freeze on corporate bank accounts.

In the 2026 era of transparent taxation, an offshore claim without economic substance is not a strategy—it is a confession. The price of compliance is high, but the price of non-compliance is now your freedom.