A Survival Guide on the New VAT Law, Foreign Investment Catalog, and Cross-Border Compliance

For Foreign-Invested Enterprises (FIEs), multinational executives, and global investors operating in China, 2026 presents a jarring paradox.

On one hand, the launch of China’s 15th Five-Year Plan (2026–2030) promises an unprecedented opening of high-value service sectors, signaling a renewed push to attract foreign capital. On the other hand, a sweeping regulatory wave—headlined by the full enforcement of the New VAT Law, the newly amended Foreign Trade Law, and the localized integration of BEPS 2.0 Pillar Two—has significantly raised the cost of non-compliance.

Many foreign operators are currently facing severe cross-border hurdles. Hidden transfer pricing exposures, aggressive audits on offshore management fees, and tightening data-export controls are causing stalled profit repatriations, customs downgrades, and unexpected tax penalties. The anxiety of asset erosion and operational disruption is no longer a distant theoretical risk—it is an immediate boardroom crisis.

To safeguard operations in 2026, foreign businesses must strategically deconstruct three pivotal legal and regulatory shifts implemented by the Chinese authorities:

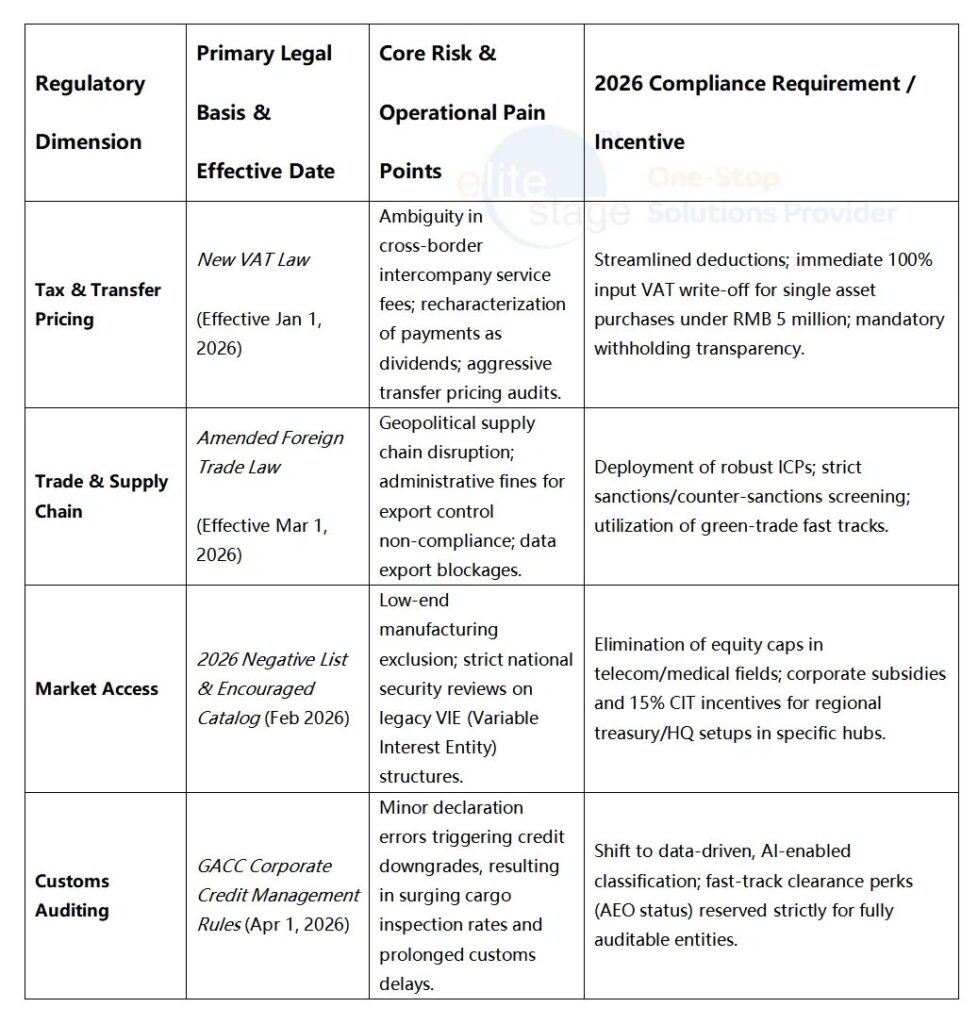

I. The New VAT Law: Strict “Withholding at Source” for Offshore Affiliates

Effective January 1, 2026, the formalized Value-Added Tax Law of the People’s Republic of China has officially replaced the decades-old provisional regulations.

● The Sourcing Rule (Place of Consumption): The law solidifies a strict destination-based principle. If an offshore parent company provides management consulting, IT support, or intellectual property (IP) licensing to a domestic Chinese subsidiary, and the services are “consumed” within China, it triggers an absolute VAT withholding obligation.

● Tightened Input Tax Deductions: The criteria for non-deductible items have been streamlined. If cross-border service agreements lack granular breakdowns of deliverables or fail to specify the exact location of service performance, domestic subsidiaries risk losing their input VAT credits entirely, leading to double taxation.

II. Amended Foreign Trade Law: Supply Chain Security Meets Trade Facilitation

Enforced as of March 1, 2026, the newly amended Foreign Trade Law codifies a dual-track approach: promoting high-standard trade digitalism while robustly enforcing national security parameters.

● Mandatory Internal Compliance Programmes (ICPs): FIEs engaged in import/export must implement rigorous compliance screenings covering export controls, dual-use items, and sanctions lists.

● Anti-Circumvention Countermeasures: The framework empowers authorities to retaliate against discriminatory foreign trade measures. FIEs caught between their home-country sanctions and China’s blocking statutes face heightened geopolitical and legal exposure.

III. Market Access “One Subtraction, One Addition”

The 2026 edition of the Negative List for Foreign Investment Access has eliminated the remaining restrictions in the manufacturing sector and systematically relaxed foreign equity caps in highly sensitive service sectors, including telecommunications, value-added healthcare, and advanced educational services.

Concurrently, the 2026 Catalog of Encouraged Industries for Foreign Investment heavily incentivizes green tech, digital economy structures, and regional headquarters setups.

⚖️ 2026 Regulatory Matrix for FIEs in China

💡 Core Steps (What to Do)

01 Restructure Intercompany Service Agreements (CSAs)

Ensure all management fees or IT allocations paid to offshore affiliates are backed by a bulletproof “substance trail.” Maintain detailed cross-border service logs, time sheets, and localized

02 Execute Localized Data Export Self-Assessments

In alignment with the Cyberspace Administration of China (CAC) 2026 updated directives, map all cross-border transfers of HR, vendor, or industrial data. File the standard contracts promptly to avoid arbitrary operational halts under data security frameworks.

03 Leverage Regional Subsidies for Structural Hedging

Consider routing investments through designated free trade zones or tech hubs (e.g., the Greater Bay Area or Shanghai FTZ), where local governments offer cash incentives (up to 1%–3% of actual utilized foreign capital, capped at RMB 50 million) alongside optimized Double Taxation Agreements (DTAs) via Hong Kong or Singapore.

⚠️ Crucial Don’ts (What to Avoid)

● Don’t rely on outdated “two-book” accounting or unbenchmarked transfer pricing. China’s Golden Tax System Phase IV is fully operational in 2026, executing deep data-matching across banking, customs, and tax networks. Arbitrary profit shifting will trigger immediate anti-avoidance audits.

● Don’t overlook Tier-2 and Tier-3 domestic suppliers. Under the amended Foreign Trade Law, if a supplier down your domestic value chain falls afoul of China’s export control or environmental red lines, your export licenses can be suspended by association.

In 2026, high-standard regulatory compliance in China is no longer an optional corporate ‘add-on’—it is the ultimate license to operate. To capture the dividends of China’s newly liberalized service sectors, multinational corporations must embed bulletproof tax and supply chain compliance directly into their structural architecture.