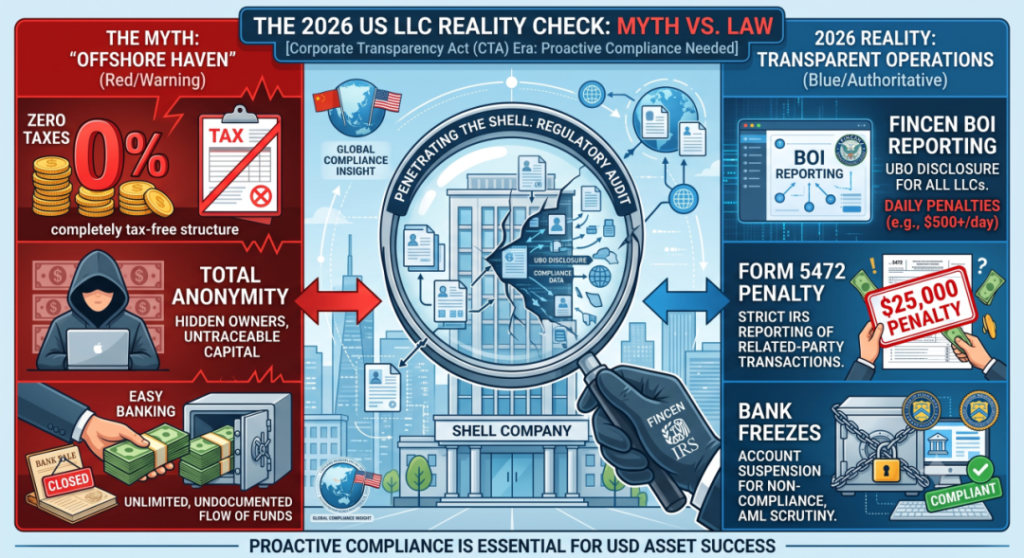

Navigating the 2026 US LLC Compliance Crackdown !

“I heard that registering an LLC in Wyoming or Delaware guarantees a zero-tax structure and access to premium USD bank accounts, as long as I don’t physically operate in the US.”

If your cross-border enterprise is still operating under this outdated assumption, the 2026 compliance storm will be a severe wake-up call.

Driven by the Financial Crimes Enforcement Network’s (FinCEN) stringent, normalized enforcement of the Corporate Transparency Act (CTA) and the IRS’s aggressive auditing of Non-US Residents, the traditional logic of the “invisible” and “tax-free” US offshore structure has been completely dismantled. Not only is it becoming increasingly difficult to open business bank accounts, but a massive wave of existing accounts are currently being frozen due to compliance reporting failures.

【Policy Explanation】

The US regulatory landscape in 2026 demands complete transparency. The dual forces of FinCEN and the IRS have established a new baseline for foreign-owned entities:

1. The 2026 BOI Reckoning: “Penetrative” Supervision

Many foreign entrepreneurs who registered US LLCs over the past few years have completely ignored FinCEN’s mandatory reporting metrics.

- Ultimate Beneficial Owner (UBO) Transparency: In 2026, whether your LLC is newly established or a legacy entity, you must unconditionally disclose the true identity of the UBO. Historical loopholes of masking shareholder identities through offshore trusts or multi-layered BVI structures are now entirely obsolete. Failure to file, or providing false information, triggers civil penalties of $500 per day and potential criminal penalties of up to 2 years in federal prison.

- The Global Information Exchange Reality: While the US is not a CRS signatory, its robust cross-border judicial collaborations and the “reverse application” of the Foreign Account Tax Compliance Act (FATCA) ensure that offshore assets can no longer hide in the dark.

2. Shattering the Tax-Free Illusion: ETBUS and the 5472/1120 Minefield

A US LLC is a “Pass-Through Entity,” meaning the company itself does not pay corporate income tax. However, this does not exempt foreign owners from filing obligations.

- The ETBUS Threshold: If your LLC has any “economic substance” within the United States—such as utilizing US-based warehouses, local fulfillment centers, domestic agents, or even hiring US-based independent contractors—it will be classified as “Engaged in Trade or Business in the US” (ETBUS). Once triggered, foreign owners are subject to federal income tax rates of up to 37%.

- Form 5472 for Non-US Residents: Even if you have zero local US business operations, a Foreign-Owned Single-Member LLC must strictly file Form 1120 and Form 5472 with the IRS in 2026. The baseline penalty for failing to file or maintaining inadequate records has surged to $25,000.

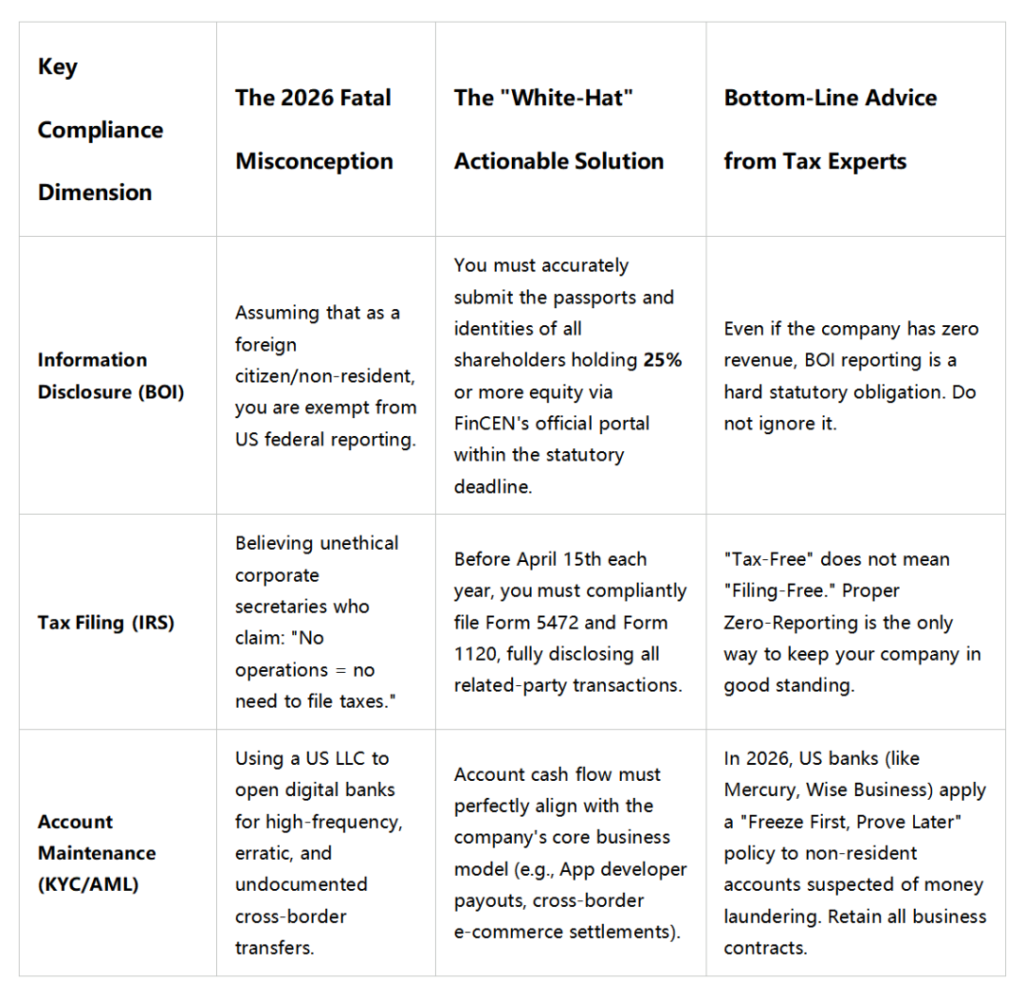

【Practical Suggestions】

💡 Bonus: Visualizing the 2026 LLC Risk Matrix

Faced with aggressive oversight, cross-border business owners and global developers cannot afford to adopt a “set it and forget it”mentality. Below is the 2026 US LLC structure self-audit and compliance guide:

There is no such thing as a free lunch in global commerce, nor is there a permanent “regulatory haven.” In the 2026 global compliance landscape, a US LLC is no longer an invisibility cloak. Only through transparent operations and rigorous, proactive reporting—guided by professional architects—can foreign entrepreneurs truly reap the rewards of USD asset allocation.