E-fapiao, as the name suggests, is a type of fapiao in electronic form. It has the same purpose and legal effect as the conventional paper fapiao.Despite the similar appearance of an e-fapiao and the scanned copy of a paper fapiao, the two are different in nature:E-fapiao is a data file that is generated in the official tax system in a structured format. It is easier for financial systems to comprehend, book, and archive automatically. And it adopts technical anti- counterfeiting measures, such as electronic signature, to ensure its authenticity.The scanned copy of a paper fapiao just mirrors information of the corresponding paper fapiao and doesn’t contain the original anti-counterfeiting measures possessed by the paper fapiao, which are mainly physical measures, such as special printing ink, the printing font, the company fapiao chop, etc. It can’t be regarded by the tax bureau as an “original” fapiao in the way the e-fapiao can be.Similar to paper fapiao, e-fapiao are also divided into two types: general VAT e-fapiao and special VAT e-fapiao, but in contrast to paper fapiao for which multiple duplicate copies are issued via the special printer, e-fapiao (whether general or special versions) only exist as a single data file. Examples of e-fapiao are shown below.

2.Advantages of e-fapiaoBecause of the digital nature of e-fapiao, it comes with added benefits for both taxpayers and tax administration.

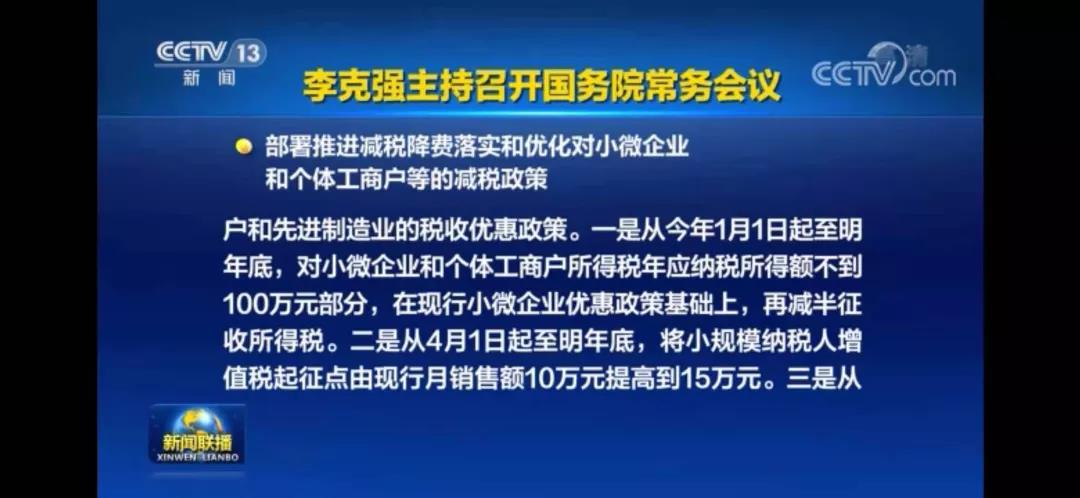

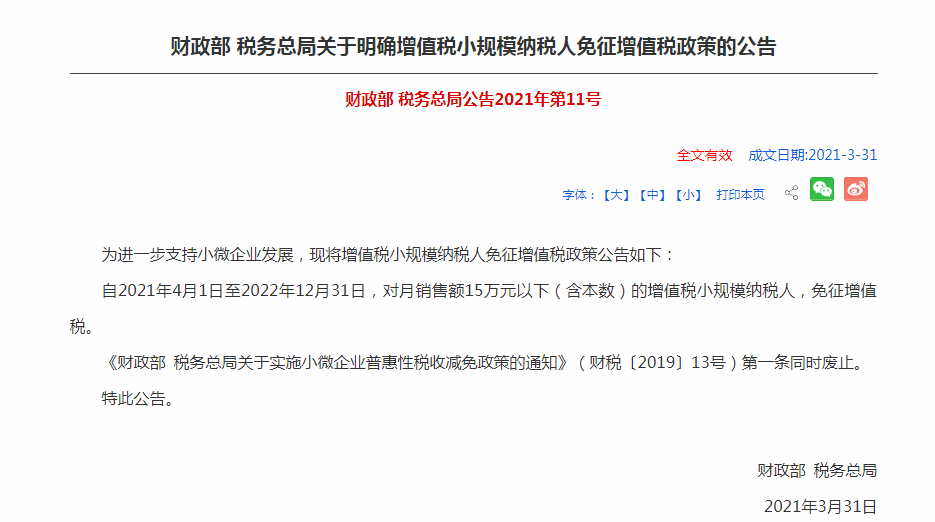

Being easier to obtain, issue, deliver, and store, the new invoicing process will lead to more cost-effective environmentally friendly business practices. Besides, considering e-fapiao is easier to search for at a later date, to retrieve when needed, and more suitable for automation, 1、小规模纳税人发生增值税应税销售行为,合计月销售额未超过15万元(以1个季度为1个纳税期的,季度销售额未超过45万元,下同)的,免征增值税。小规模纳税人发生增值税应税销售行为,合计月销售额超过15万元,但扣除本期发生的销售不动产的销售额后未超过15万元的,其销售货物、劳务、服务、无形资产取得的销售额免征增值税。

2、适用增值税差额征税政策的小规模纳税人,以差额后的销售额确定是否可以享受本公告规定的免征增值税政策。《增值税纳税申报表(小规模纳税人适用)》中的“免税销售额”相关栏次,填写差额后的销售额。

3、按固定期限纳税的小规模纳税人可以选择以1个月或1个季度为纳税期限,一经选择,一个会计年度内不得变更。

4、《中华人民共和国增值税暂行条例实施细则》第九条所称的其他个人,采取一次性收取租金形式出租不动产取得的租金收入,可在对应的租赁期内平均分摊,分摊后的月租金收入未超过15万元的,免征增值税。

5、按照现行规定应当预缴增值税税款的小规模纳税人,凡在预缴地实现的月销售额未超过15万元的,当期无需预缴税款。

6、小规模纳税人中的单位和个体工商户销售不动产,应按其纳税期、本公告第五条以及其他现行政策规定确定是否预缴增值税;其他个人销售不动产,继续按照现行规定征免增值税。

7、已经使用金税盘、税控盘等税控专用设备开具增值税发票的小规模纳税人,月销售额未超过15万元的,可以继续使用现有设备开具发票,也可以自愿向税务机关免费换领税务Ukey开具发票。

8、本公告自2021年4月1日起施行。《国家税务总局关于小规模纳税人免征增值税政策有关征管问题的公告》(2019年第4号)同时废止。 more streamlined, efficient, and accurate with improved data quality. The business environment and general market vitality can be expected to be improved as a consequence.

3. Why does it matter?

小规模纳税人起征点月销售额标准提高以后,销售额的执行口径是否有变化?

没有变化。

纳税人确定销售额有两个要点:

一是以所有增值税应税销售行为(包括销售货物、劳务、服务、无形资产和不动产)合并计算销售额,判断是否达到免税标准。但为剔除偶然发生的不动产销售业务的影响,使纳税人更充分享受政策,本公告明确小规模纳税人合计月销售额超过15万元(以1个季度为1个纳税期的,季度销售额未超过45万元,下同),但在扣除本期发生的销售不动产的销售额后仍未超过15万元的,其销售货物、劳务、服务、无形资产取得的销售额,也可享受小规模纳税人免税政策。二是适用增值税差额征税政策的,以差额后的余额为销售额,确定其是否可享受小规模纳税人免税政策。举例说明:按季度申报的小规模纳税人A在2021年4月销售货物10万元,5月提供建筑服务取得收入40万元,同时向其他建筑企业支付分包款12万元,6月销售不动产200万元。则A小规模纳税人2021年第二季度(4-6月)差额后合计销售额238万元(=10+40-12+200),超过45万元,但是扣除200万元不动产,差额后的销售额是38万元(=10+40-12),不超过45万元,可以享受小规模纳税人免税政策。同时,纳税人销售不动产200万元应依法纳税。Attention:E-fapiao is related to all businesses E-fapiao will affect businesses sooner than expected E-fapiao has imposed new compliance requirements on the financial and accounting processes E-fapiao requires software installment and system upgrade E-fapiao will affect businesses sooner than expected E-fapiao offer a great opportunity for enterprises to further automate and optimize their operationsPlease note that not only the financial and accounting processes will be affected. The implementation of e-fapiao and associated improved automation will also help to optimize other key operations, such as supply chain management, client relationship management, reporting, etc.In the context of the tax bureau’s determination to achieve advanced tax administration through information technology, the implementation of e-fapiao is imperative. The digital nature of e-fapiao will bring multiple benefits to businesses in achieving higher accuracy, higher efficiency, and higher levels of automation.However, on the other hand, the e-fapiao implementation also impose challenges on businesses in the short-term to understand the laws and regulations, develop relevant internal protocols, revise standard business processes, and upgrade relevant software and equipment to comply with the new reimbursement, bookkeeping, and archiving requirements.It’s important that companies get prepared and develop a thorough strategy for e-fapiao to alleviate operational risks and get the most out of the e-invoicing trend.

Please note that not only the financial and accounting processes will be affected. The implementation of e-fapiao and associated improved automation will also help to optimize other key operations, such as supply chain management, client relationship management, reporting, etc.In the context of the tax bureau’s determination to achieve advanced tax administration through information technology, the implementation of e-fapiao is imperative. The digital nature of e-fapiao will bring multiple benefits to businesses in achieving higher accuracy, higher efficiency, and higher levels of automation.However, on the other hand, the e-fapiao implementation also impose challenges on businesses in the short-term to understand the laws and regulations, develop relevant internal protocols, revise standard business processes, and upgrade relevant software and equipment to comply with the new reimbursement, bookkeeping, and archiving requirements.It’s important that companies get prepared and develop a thorough strategy for e-fapiao to alleviate operational risks and get the most out of the e-invoicing trend.

Please note that not only the financial and accounting processes will be affected. The implementation of e-fapiao and associated improved automation will also help to optimize other key operations, such as supply chain management, client relationship management, reporting, etc.In the context of the tax bureau’s determination to achieve advanced tax administration through information technology, the implementation of e-fapiao is imperative. The digital nature of e-fapiao will bring multiple benefits to businesses in achieving higher accuracy, higher efficiency, and higher levels of automation.However, on the other hand, the e-fapiao implementation also impose challenges on businesses in the short-term to understand the laws and regulations, develop relevant internal protocols, revise standard business processes, and upgrade relevant software and equipment to comply with the new reimbursement, bookkeeping, and archiving requirements.It’s important that companies get prepared and develop a thorough strategy for e-fapiao to alleviate operational risks and get the most out of the e-invoicing trend.