Navigating the 2026 Cross-Border Compliance Tide: The End of “Shell” Companies in Hong Kong vs. Singapore

As we progress through July 2026, the global tax landscape has definitively shifted under the weight of the BEPS 2.0 era.

Multinational enterprises (MNEs) and high-net-worth investors are facing an unprecedented regulatory crackdown. The historical strategy of relying on empty offshore structures to optimize tax liabilities is officially obsolete.

Both Hong Kong and Singapore have radically tightened their compliance frameworks, leading to increased reporting burdens, aggressive scrutiny, and elevated compliance costs for foreign business owners. If your regional headquarters cannot prove genuine local activity, your enterprise is exposed to severe financial and regulatory risks.

The projected 2026 regulatory landscape demonstrates a synchronized effort by Hong Kong (HKIRD) and Singapore (IRAS) to enforce strict economic substance and minimum tax standards. Most notably, both jurisdictions have adopted Pillar Two implementations, which mandate a 15% global minimum tax applicable to specific MNE groups generating over €750m in revenue.

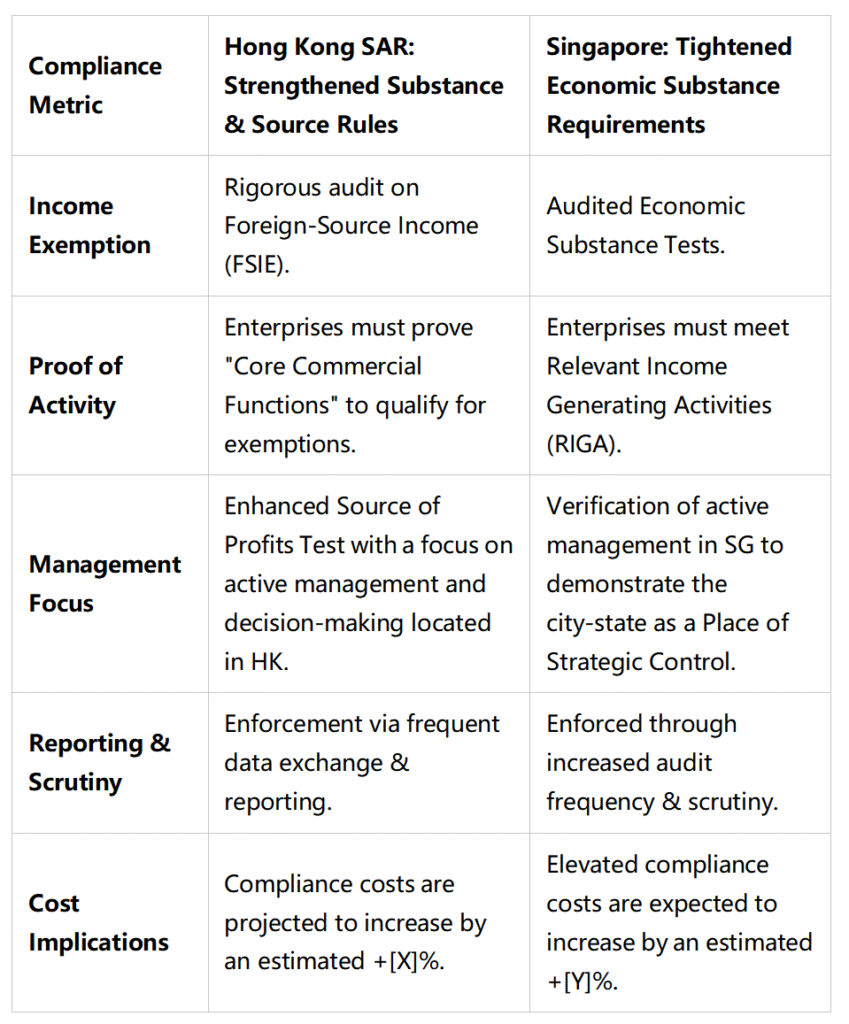

However, their specific operational audits differ. Below is a critical comparison of how both hubs are enforcing the new rules:

To survive the 2026 compliance new norm, business owners must transition from passive structuring to active operational management. Implement the following business preparation checklist immediately:

1. Review Group Structure: You must rigorously evaluate your corporate architecture to ensure all entities meet substance tests and carefully monitor BEPS thresholds.

2. Map Functions, Assets, Risks: Do not rely on paper directors; validate that your core functions are genuinely being performed locally.

3. Enhance Data Collection & Verification: Upgrade your internal systems to prepare granular compliance data, as regulatory bodies now demand highly detailed evidence of operations.

4. Seek Professional Cross-Border Advice: Engage specialized consultants to structure your operations optimally and mitigate emerging cross-border risks.

In the BEPS 2.0 era, operational substance is no longer merely a bureaucratic checkbox; it is the definitive baseline for corporate survival and cross-border wealth protection.