2026 Trump China Summit How Global Entrepreneurs Can Seize the Opportunity

In 2026, Donald Trump’s visit to China is not merely a “nuclear-level” geopolitical event; it is a high-stakes “stress test” for the profit margins of thousands of global enterprises.

While news cycles are saturated with talk of tariff hikes, tech blockades, and “decoupling,” a deep-seated anxiety has gripped entrepreneurs in e-commerce, new energy, and smart manufacturing. The questions are haunting: “Is the U.S. market still viable?” “Should I pull my entire supply chain out of China?”

However, for those with a keen eye for capital flow, focusing solely on “crisis” means missing the greatest redistributive dividend of the next five years. The essence of the U.S.-China game is shifting from “Direct Confrontation” to “Rule Reshaping.” For the agile entrepreneur, the short-term volatility triggered by this summit is precisely the Golden Window for global supply chain restructuring and capital arbitrage via offshore springboards.

【Strategic Deconstruction】

Peeling back the political fog, we must look at the “Capital & Tax” underlying logic to see the tangible opportunities:

1. The “Springboard Reconstruction” under Tariff Pressure

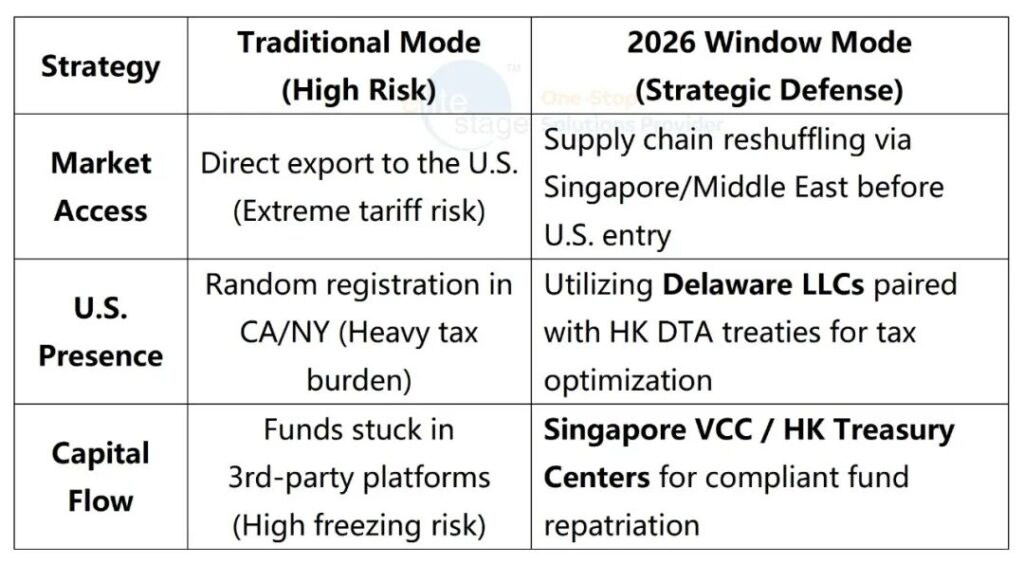

Trump’s “America First” policy and push for reshoring manufacturing are constants. If the summit yields partial tariff exemptions or phased agreements, this is not a signal to continue shipping directly from China. Instead, it is a grace period to build the “Golden Triangle” architecture: China HQ + SE Asia/Mexico Assembly + U.S. Local Sales.

● The Shift: We are witnessing an evolution from “Made in China” to a sophisticated “Owned by China” global capital layout.

2. Tax Dividends in U.S. “Tax-Friendly States”

To bypass trade barriers, establishing a local U.S. entity (C-Corp or LLC) has become a necessity rather than an option.

● The Opportunity: Savvy entrepreneurs are leveraging “Tax Havens” within the U.S. (such as Delaware, Wyoming, or Nevada) to set up holding entities that enjoy exemptions from state income tax. Combined with offshore structures in Hong Kong or Singapore, this allows for legal profit carving and tax deferral on a global scale.

3. Cross-Border M&A and Bottom-Fishing

Heightened friction often leads multinational corporations to restructure or divest non-core assets. For high-net-worth individuals with Family Offices (VCC structures) in Singapore or liquid offshore pools in Hong Kong, 2026 represents a prime node to use strong foreign currency for low-cost asset acquisition and global diversification.

Strategic Comparison: The 2026 Pivot

【Actionable Advice】

Recommendation 1: Use a “Double-Layer Structure” to Isolate Compliance Risks

Never allow a Chinese parent company to hold a U.S. entity directly. In the event of U.S. litigation, this can lead to the “piercing of the corporate veil,” putting domestic assets at risk.

● The Blueprint: Establish a Hong Kong/Singapore Holding Co. (with proper ODI filing) $\rightarrow$ which then holds the U.S. Delaware Entity. This creates a professional “firewall” that leverages tax treaties while isolating the unlimited liability of the U.S. market.

Recommendation 2: The Dubai (Middle East) “Plan B”

The outcome of the Trump-China summit remains unpredictable. Do not put all your eggs in one basket. In 2026, utilizing Dubai’s low operational costs and Zero-Tax Free Zones provides a cost-effective “Plan B” for logistics and capital clearing when targeting the Western hemisphere.

Pitfall Warning: Beware the “Country-of-Origin” Red Line

Do not attempt to bypass tariffs by simply “repackaging” goods in Southeast Asia. U.S. Customs and Border Protection (CBP) is extremely rigorous regarding “Rules of Origin.” You must ensure “Substantial Transformation” or significant value-added processing occurs in the third country to legally navigate tariff barriers.

The 2026 summit is a fork in the road. Will you be a casualty of the trade war, or the architect of a new global capital map? The window is open, but it won’t stay that way for long.